Gross domestic product (GDP) measures total output in the domestic economy. Nominal GDP, real GDP and potential GDP are three different measures of aggregate output. Nominal GDP is the market value all final good and services produced in the domestic economy in a ONE YEAR period at current prices. By this definition,

(1)only output exchanged in a market is included (do-it - yourself services such as cleaning your own house are not included)

(2) output is valued in this final form (output is in it final form when no further alteration is made to the good which would change its market value.

(3) output is measured using current year prices.

Because nominal GDP values are inflated by prices that increase over time, aggregate output is also measured holding the prices of all goods and services constant over time. This valuation of GDP at constant prices is called REAL GDP.

the third measure of aggregate output is potential GDP, the maximum production that can take place in the domestic economy without creating upward pressure on the general level of prices. Conceptually,potential GDP represents a point on a given production possibility frontier.

The US economy's potential output increases at a fairly steady rate each year while actual real GDP fluctuates around potential GDP. The fluctuation of the real GDP are identified as business cycles. The GDP gap is the difference between the potential GDP and real GDP; it is positive when potential GDP exceeds real GDP and negative when real GDP exceeds potential GDP. A positive gap indicates that there are unemployed resources and the economy is operating inefficiently within its production possibility frontier. It therefore follows that an economy's rate of unemployment rises as its GDP gap increases and falls when the gap declines.An economy is operating above its normal productive capacity when there is a negative gap.

Sunday, February 21, 2010

Monday, November 30, 2009

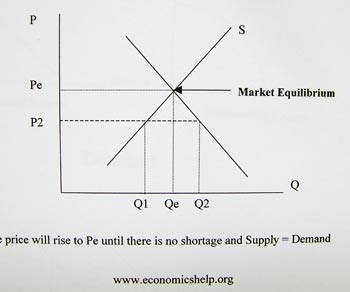

Equilibrium Price and Quantity

Equilibrium occurs at the intersection of the market supply and market demand curves.At this intersection, quantity demanded equals quantity supplied ie., the quantity producers and willing to supply. A surplus exists at prices higher than the equilibrium price since the quantity demanded falls short of the quantity supplied. At price lower than the equilibrium price, there is a shortage of output since quantity demanded exceeds quantity supplied.Once achieved,the equilibrium price and quantity persist until there is a change in demand and/or supply.

Equilibrium price and/or equilibirum quantity change when the market demand and/or market supply curves shift. Equilibrium price and equilibrium quantity both rise when there is an increase in market demand with no change in market supply curve.Equilibrium price falls while equilibrium quantity increases when market supply increases and demand is unchanged.

Thursday, November 12, 2009

Supply

A supply specifies the units of a good or service that a producer is willing to supply (Qs) at alternative prices over a given period of time.i.e Qs = f (P). The supply curve normally has a positive (upward) slope, indicating that the producer must receive a higher price for increased output due to the principle of increasing costs. A market supply curve is derived by summing the units each individual producer is willing to supply at alternative prices. A typical market supply curve :-

The supply curve above shows the changes on the quantity supplied. An increase in the quantity supplied by firms shifts the supply curve rightward,whereby a decrease will see a backward shift.

The market supply curve shifts when the number and/or size of producers changes,factor prices such as interest,wages, rent paid to economic resources change,the cost of materials,technological progress occurs, and/or the government subsidization(To be explained soon). A change in supply thereby denotes a shift of supply curve. A change in quantity supplied indicates a change in the commodity's price and therefore a movement along an existing supply curve.

The supply curve above shows the changes on the quantity supplied. An increase in the quantity supplied by firms shifts the supply curve rightward,whereby a decrease will see a backward shift.

The market supply curve shifts when the number and/or size of producers changes,factor prices such as interest,wages, rent paid to economic resources change,the cost of materials,technological progress occurs, and/or the government subsidization(To be explained soon). A change in supply thereby denotes a shift of supply curve. A change in quantity supplied indicates a change in the commodity's price and therefore a movement along an existing supply curve.

Sunday, October 18, 2009

Demand

Here comes the most anticipating topic of all,the demand and supply. The demand and supply theory is a powerful yet applicable throughout the economic syllabus.

The demand schedule for an individual specifies the units of a good or service that the individual is willing and able to purchase at alternative prices during a given period of time. The relationship between price and quantity demanded is inverse: more units are purchased at lower prices because of a substitution effect and an income effect. As a commodity's price falls,an individual normally purchases more of this goods since he or she likely to substitute it for other goods whose price has remain unchanged. Also, when a commodity's price falls,the purchasing power of an individual with a given income increases,allowing for greater purchases of the commodity. When graphed, the inverse relationship between the price and quantity demanded appears as an negatively sloped demand curve.A market demand schedule specifies the units of a good or service all individuals in the market are willing and able to purchase at alternative prices. Here is a simple demand graph to demonstrate how the demand works.

When the price per unit(top) is 400pound, consumers tend to demand less for the good,whereby as the price drops,the demand for the good or services escalates. Here is an easy example,when the price of a good,let say a Playstation 3 drops about 20%,more people will start demanding for the gaming console. The market demand for a good and services are not only ''possess'' by the commodity's price, but also by the price of other goods and services,disposable income,wealth,tastes and the size of the market. The relationship is presented as ceteris paribus.

The market demand curve shifts up and to the right when there is an increased preference for the commodity ,when incomes increase, and when substitute commodities* rises and/or the price of a complementary good declines.

____________________________________________________________________

A common error made by the beginning economics student is failure to differentiate between a change in demand and a change in quantity demanded.A change in demand refers to a shift of the demand curve because a variable other than price has changed. A change in quantity demanded occurs when there is a change in the commodity's price,resulting in a movement along an existing demand curve.

Scarcity and the Market System

As we have seen, two of the most important economic decisions faced by a society are deciding what goods and services to produce and how to allocate resources among their competing uses. The combination of goods and services produced can be resolved by government command or through market system. In command economy, a central planning board determines the mix of output. The experience by the changing economic and political event in the command economies of Eastern Europe and the former USSR.

In a market economy, economic decisions are decentralized and are made by the collective wisdom of the marketplace, i.e., prices resolve the three fundamental economic questions of what,how and for whom. The only goods and services produced are those that individuals are willing to purchase at a price sufficient to cover the cost of producing them. Because resources are scarce, goods and services produced are sold(distributed) to those who are willing and have the money to pay the prices.

Most countries have a mixed economy, a mixture of both command and market economies. For example, the United States has primarily a market economy, although the government produces some goods,such as roads,and finances these expenditures by taxing the income of individuals and businesses. The government may also regulate how the market operates,such as with minimum wage laws.

Saturday, October 3, 2009

Production-Possibility Frontier(PPF)

A production possibility frontier shows the maximum number of alternative combinations of goods and services that a society can produce at a given time when there is full utilization of economic resources and technology.The production possibility frontier depicts not only limited production capability and therefore the problem of scarcity,but also the concept of opportunity cost arise.Here is a simple PPF graph.

figure 1.1

figure 1.2

However, the production possibility frontier shifts outward over time as more resources become available and/or technology is improved. Growth in an economy productive capability is depicted in figure 1.2 by the outward shift of the PPF from PP1 to PP2. Points on the PPF are considered to be efficient. Points within the frontier are inefficient,and point outside the PPF are unattainable. Positions outside the PPF are unattainable since the frontier defines the maximum amount that can be produced at a given time. Positions within the frontier are inefficient because some resources are either unemployed or underemployed.

Opportunity Cost

All decision requires opportunity costs. An opportunity cost is what is sacrificed to implement an alternative action, i.e. what is given up to produce or obtain a particular good or service. For example, the opportunity cost of expanding a country's military arsenal is the decreases production of non military goods and services. Opportunity costs are found in every situation in which scarcity necessitates decision making.

Opportunity cost is the value-monetary or otherwise-of the next best alternative,or which is given up. This concept is used in both macroeconomics and microeconomics.

Subscribe to:

Comments (Atom)