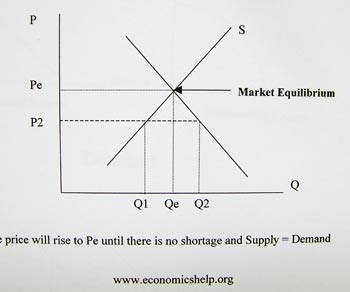

Here comes the most anticipating topic of all,the demand and supply. The demand and supply theory is a powerful yet applicable throughout the economic syllabus.

The demand schedule for an individual specifies the units of a good or service that the individual is willing and able to purchase at alternative prices during a given period of time. The relationship between price and quantity demanded is inverse: more units are purchased at lower prices because of a substitution effect and an income effect. As a commodity's price falls,an individual normally purchases more of this goods since he or she likely to substitute it for other goods whose price has remain unchanged. Also, when a commodity's price falls,the purchasing power of an individual with a given income increases,allowing for greater purchases of the commodity. When graphed, the inverse relationship between the price and quantity demanded appears as an negatively sloped demand curve.A market demand schedule specifies the units of a good or service all individuals in the market are willing and able to purchase at alternative prices. Here is a simple demand graph to demonstrate how the demand works.

When the price per unit(top) is 400pound, consumers tend to demand less for the good,whereby as the price drops,the demand for the good or services escalates. Here is an easy example,when the price of a good,let say a Playstation 3 drops about 20%,more people will start demanding for the gaming console. The market demand for a good and services are not only ''possess'' by the commodity's price, but also by the price of other goods and services,disposable income,wealth,tastes and the size of the market. The relationship is presented as ceteris paribus.

The market demand curve shifts up and to the right when there is an increased preference for the commodity ,when incomes increase, and when substitute commodities* rises and/or the price of a complementary good declines.

____________________________________________________________________

A common error made by the beginning economics student is failure to differentiate between a change in demand and a change in quantity demanded.A change in demand refers to a shift of the demand curve because a variable other than price has changed. A change in quantity demanded occurs when there is a change in the commodity's price,resulting in a movement along an existing demand curve.